Worst-case scenario for the Israel-Iran conflict

In this continuously updating blog we map the worst-case scenario

In this continuously updating blog we map the worst-case scenario

Our December 2021 special report on the Great Reset included

Some think that the arrival of economic crises, or economic

Asset markets in the U.S. are flirting with a ‘bear

Something that many thought could not happen in our lifetime

During this year, we have awakened to a completely new

We have been highly critical of the ‘unorthodox policies’ of

In the March issue of our Q-Review series we warned

We continue our financial history series by going through the

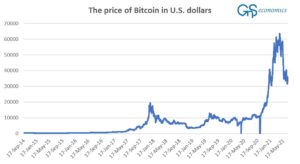

Cryptocurrencies have experienced a remarkable rise in numbers and popularity

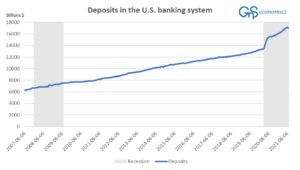

Banking is at the heart of modern economic systems. The