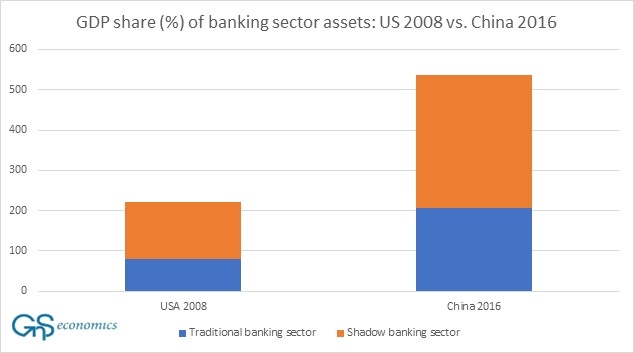

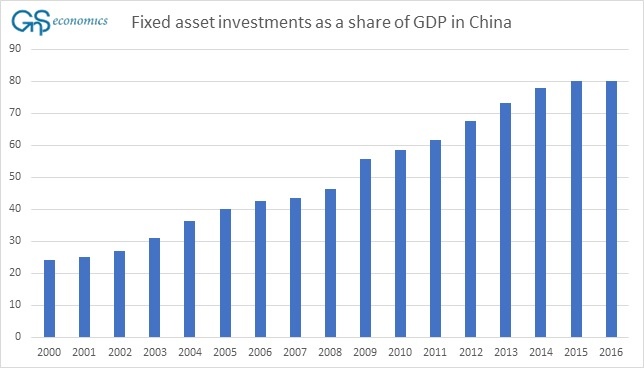

Economists have been somewhat slow to see the threat of China on the global economy, the threat we have been warning since March. Within the last two months, however, the debate has changed a lot. S&P cut China’s credit rating and even the IMF warned about the risks of China. The problems of China can be summarized in two figures indicating that the economy of China is both over-levered (see figure 1) and over-invested (see figure 2 below).

Figure 1. The share (%) of the assets of traditional and shadow banking sectors to GDP in China in 2016 and in the US in 2008. Source: GnS Economics, FRBNY, BIS, PBoC

Figure 2. Investments actually completed in fixed assets as a share of GDP (%) in China. Source: GnS Economics, NBS of China

The interesting question is whether China will change its economic policy after the 19th Congress of the Communist Party of China opening on 18 October? Will it restrain credit creation and start to crack-down the dubious financial practices or will it continue with its current policy line?

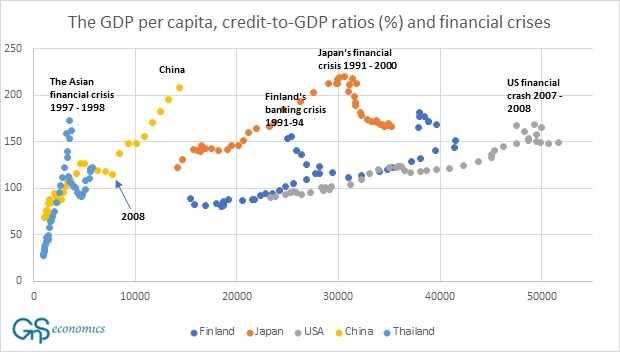

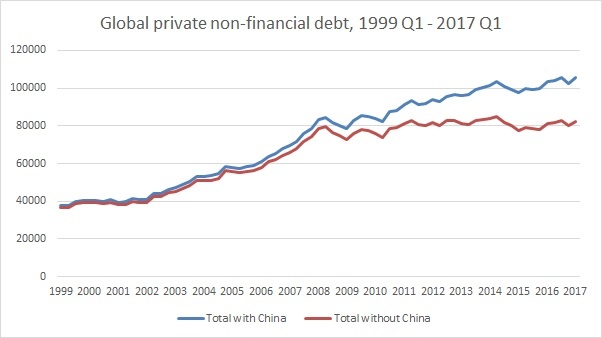

Both alternatives are possible. The growth of credit in China has been enormous since 2008 (see figure 3 below) and China has actually been the sole source of global private credit growth (see figure 4 below). Because the private debt grows around three times as fast as GDP, it is evident that China cannot continue on this path much longer, but will it keep going till the bitter end? In early 2016, for example, China planned a shift from investment-led to consumption-driven growth. The experiment pushed China towards a recession. The rapid economic decline apparently spooked the leaders who enacted a massive debt-driven stimulus. The economy of China bounced back and lifted the world economy on the verge of a serious downturn.

Next week, Xi Ping will most likely be re-elected for another five-year term. When he was first elected in 2012, he was expected to bring a more market-oriented and debt growth-constraining policies. In his first term, these hopes were somewhat dashed. His policy towards corruption has been harsh but it has not been very market-friendly. The draconian capital control issued lately is a distinct example of this. Why would he change the course this time?

Figure 3. The GDP per capita (horizontal), credit-to-GDP ratios for non-financial private sector (vertical) and financial crises. Source: GnS Economics, BIS, World Bank

Figure 4. Non-financial debt of the private sector in 44 major countries. In billions of US dollars. Sources: GnS Economics, BIS.

Despite of this well-founded skepticism, there are some signals from the possibility of the coming change. Several times during this year, Xi has warned about the risks of the global economy, most recently in September. As the Chinese government prefers to take only cautious steps, these warnings almost surely serve some purpose. Of what exactly, remains to be seen.

Other, nearly missed signal came in a form of a research. Jun Nie, a senior researcher at the Federal Reserve Bank of Kansas City and Yandong Jia, a researcher at the Research Bureau of the People’s Bank of China (PBoC), recently published an article that painted a bleak picture of the future growth prospect of the economy of China. It is almost unheard of that a member of PBoC publicly criticizes the sustainability of China’s economic growth. It could be interpreted as a signal from a change in the policy.

What will China do? China prefers stability, but are they willing to allow for short-term instability to sustain long-term goals? No one knows. Nevertheless, one thing is certain: China cannot grow out of its mountain of debt. Thus, a hard landing seems unavoidable, and the world should be prepared for it.

Errata in the last paragraph corrected 6/12/2018.

Keep up-to-date on developments in China and policies of central banks as well on growing risks in the global markets through our Q-Review -reports. The annual subscription (4 issues) is available atGnS Store