Whatever has the nature of arising, has the nature of ceasing.

– Buddha (attributed)

We have not been living through a typical business cycle. It has puzzled us since the publication of our first warning on the possibility of a global crash in March 2017 why the true nature of the current economic expansion remains so elusive to many.

While the acute phase of the crisis ended in 2009 when the global economy started to recover, the pervasive and extraordinary efforts to support the global economy and global capital markets have only begun to be curtailed to any serious degree this past year. As we have seen, this has already started to create serious market and economic turmoil, and more is on the way.

“Ask, and it will be given to you”

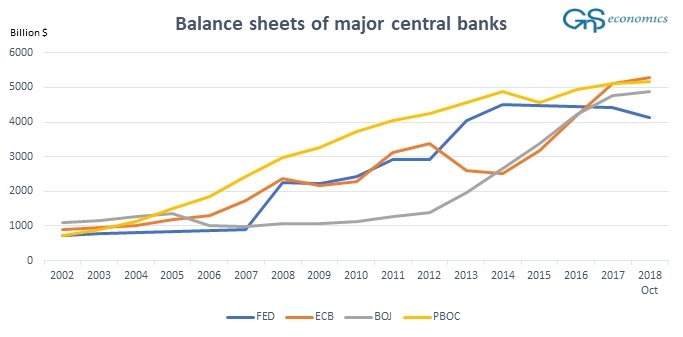

After the crisis, central bankers took a direct, pronounced and active role in the capital markets to an extreme never assumed before. Whenever there was a problem, they threw money at it to make it go away. Their balance sheets ballooned (see Figure below). China, for its part, enacted record-breaking debt stimulus to support its economy whenever it “hiccupped”, which also supported the global economy. Effectively, central banks and governments became the persistent counterweight to any tendency to economic weakness or market losses.

Figure. The balance sheets of the Bank of Japan, European Central Bank, Federal Reserve and the People’s Bank of China in billions US dollars. Source: GnS Economics, BoJ, ECB, Fed, PBoC

Here is a (non-comprehensive) list of the main “stop-loss” operations by major central banks and governments:

- When the financial crisis hit in 2008, China wasted no time in reacting by employing vast credit and infrastructure stimulus programs. Beijing explicitly ordered banks to ramp up lending, and the banks responded by doubling the volume of loans YoY. Between 2007 and 2015, 63% of all new money created globally came from China, and most of this increase was created by commercial banks. This massive credit stimulus carried the world economy, and especially Europe, into a fast recovery from a rather deep recession.

- In late November 2008, the U.S. Federal Reserve (Fed) announced it would start buying the debt of Government Sponsored Enterprises (“GSE”) and mortgage-related securities in the secondary market. In March 2009, the Fed extended the program to include U.S. Treasuries. These became known generically as the program of quantitative easing or “QE”. The Fed ran three sequential QE programs of which the last was concluded (ending net purchases) in October 2014. All the major central banks followed the Fed’s example with the Bank of England starting its QE program in March 2009, the Bank of Japan (BoJ) in October 2010 (for the second time), the European Central Bank (ECB) in March 2015 and the People’s Bank of China (PBoC) in July 2015. These programs affected the financial markets in numerous ways.

- In October 2010, the BoJ started to buy Exchange Traded Funds (“ETF”) linked to the Japanese stock market. It became customary that the BoJ would begin buying whenever the Topix stock market index fell more than a 0.2 percentage points by midday. Currently, the BoJ holds around 75% of the ETF universe in Japan and around 4 percent of the market value of the stocks traded on the Tokyo Stock Exchange. It has become the leading shareholder in several large Japanese companies.

- In August 2012, the European Central bank enacted the Outright Monetary Transactions program to halt the rise in sovereign yields in the Eurozone.

- In 2015, the Chinese economy started to roll over. Stock markets and real estate prices began falling. Authorities panicked and doubled-down. They directed funds to investments through the shadow banking sector which led to an unprecedented credit spree. In just one year, assets in the shadow banks exploded three-fold bringing the private debt-to- GDP ratio in China to an astronomical 545 percent.

- Also in 2015, in an effort to devalue the Swiss Franc, the Swiss National Bank started to “invest” in foreign assets, including U.S. equities. The SNB currently holds around $88 billion worth of U.S. equities and it is a significant shareholder of blue-chip American multinationals such as Apple, Exxon-Mobil and Procter & Gamble. In many cases, such purchases by the SNB coincided with increased market turbulence/risk, as during the first actual rate hike cycle of the Fed in 2016/2017. Whether these were related or not remains unknown at this point.

- 2017 set the record for central bank stimulus. During that year, central banks across the globe pushed over $2 trillion worth of artificial central bank liquidity into the global markets in an ‘Liquidity Supernova’.

- In 2018, President Trump boosted the economy with a massive, late-cycle fiscal stimulus package by cutting personal and especially corporate tax rates (from 35 to 21 percent). This led to a further wave of stock buybacks, the repatriation of foreign capital holdings of US companies and an acceleration in capital expenditures by firms. These supported both the stock market, corporate earnings and the real economy. However, the balance sheet reduction (quantitative tightening, or “QT”) program of the Fed countered these initiatives to some extent and also helps to explain the increased volatility in U.S. stock markets over the course of 2018 (see Q-review 1/2018).

This massive and unprecedented monetary meddling and deficit-spending stimulus has naturally led to serious misallocations in the capital markets and to the crowding-out of private investments in the economy. Alas, the global economy has become both ‘zombified’ and fragile.

The end

Economic expansions can be viewed as children. They come with their own genetic makeup which, in combination with how they are raised, will define how they behave and end up as adults. This expansion in its own way was a misbegotten mix of moral hazard, leverage, regulatory failures and massive speculation. A bastard. It was spoiled with easy money and by smoothing every nasty shock with more easy money. Alas, it is not able to stand on its own and will collapse without support.

In economic terms, central bankers and governments have supported the world economy with tens of trillions of dollars, created ex-nihilo. There has never been such an extraordinary level of stimulus in history. That is why this is, by definition, the most manipulated business cycle—ever. When the stimulus is removed, the world economy will collapse under the weight of debt and mis-priced financial risk.

When the Fed started QT in October 2017, and China started to rein-in its shadow banking sector around the same time, the countdown for the end of this manipulated business cycle started. These measures have already led to emerging market troubles, a harrowing rise in Libor and the return of stock market volatility. In the near future, they will lead to

- a global slowdown,

- an asset market crash, and ultimately to

- a global depression.

There’s very little than can be done to avoid all this. While major central banks and governments may be able to postpone the inevitable for a while longer, they have birthed and then nurtured a monster, a dangerous economic mutant which will collapse and take the world economy with it. It’s time. to prepare

Full report describing the scenarios depression could take, their probabilities, growth forecasts and a description of the eventual recovery of the world economy is available atGnS Store

Annual subscription (4 issues) of our reports (Q-reviews) is now available atGnS Store