Subscribe to our Newsletter.

The Stage of the Crisis: The beginning of the Flood

Updated 11/11/2023 (The U.S. banking system and looming war in the Middle East). All updates are presented in bold.

In the December 2018 issue of our Q-Review, we outlined the likely scenarios of an approaching global economic collapse. But, like most things in life, such a dramatic event is unlikely to proceed in a purely linear fashion. There will be different stages within it.

In December 2019 we outlined these stages, which are likely five: the Onset, Counter-attack, Flood, Calamity and Recovery. Here, we briefly define the characteristics of each, updating them with recent information.

The Onset of the Crisis

In the Q-Review 4/2019, we specified that at the Onset, stresses that had been building in the credit markets since the summer of 2019 would explode, shrinking if not eliminating entirely the exits from many parts of that market. Downgrades of corporate debt in the U.S. and peripheral sovereign debt in the Eurozone would push large fixed-income investors, including pension funds, into higher-rated bonds, which would in turn lead to large-scale selling of lower-rated bonds, forcing wider spreads and even more selling.

This moment came in late February 2020, when a sudden panic gripped investors in both credit and equity markets after a surge in reported Covid-19 cases and deaths in Italy coincided with the collapse of OPEC talks. Stock markets crashed and spreads in the credit markets exploded. A frantic retreat to ‘safe-haven’ assets, including U.S. Treasuries, German Bunds and U.K. Gilts as well as cash and precious metals commenced.

For a brief period of time in mid-March 2020, we were on the brink of a complete financial market meltdown. Then, as we also had envisaged in December, there was a frantic rush, a Counterattack, on a never-seen-before scale by global and local authorities to rescue the situation.

The Counterattack

We envisaged that the second phase of the collapse would be the desperate efforts of authorities to stop the crisis by a counterattack. We said these were likely to include the restarting and acceleration of QE programs and other market support initiatives, gigantic fiscal stimulus, increasing trade protectionism and possibly even calls for direct debt monetization (see Q-Review 3/2019 for an explanation).

These tactics were employed in full force. Governments all over the world pushed vast amounts of debt-financed stimulus into their respective economies. During the spring of 2020 this manifested through both never-before-seen government and central bank support of the financial sector and the real economy.

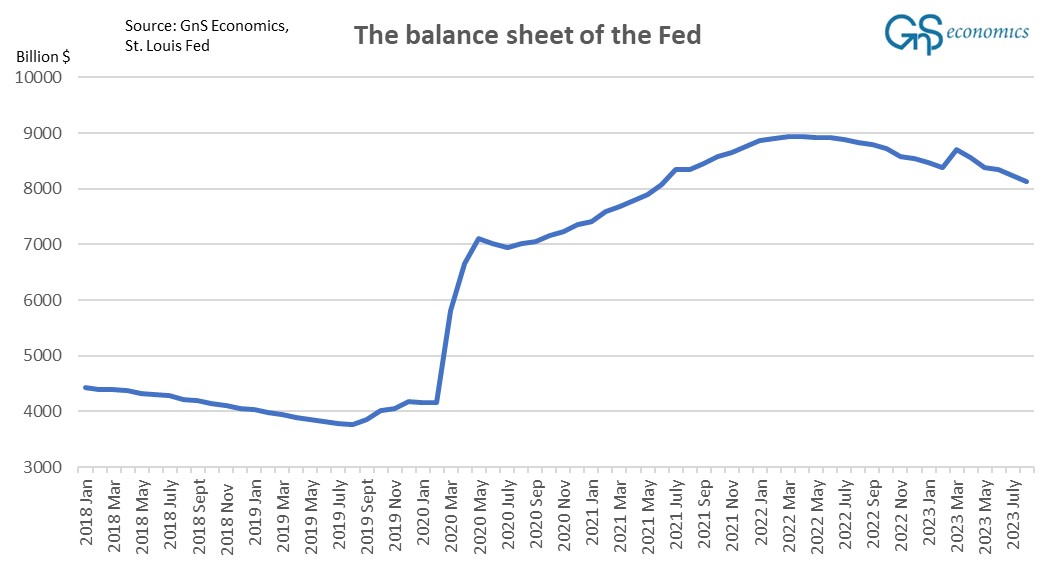

Moreover, during the spring of 20202, the Fed effectively became the financial market (see Figure 1) as it backstopped U.S. Treasury markets, intervened in corporate commercial-paper and municipal bond markets and short-term money-markets. Massive support by the FED and the “free money”-schemes of the government levitated U.S. stock market valuations to levels not seen since, at least, the height of the “Tech Boom” in 1999.

During the spring of 2020, the ECB increased its ‘Pandemic Emergency Purchase Program’ to a €1,850 billion behemoth, and the European leaders reached an agreement on the €750 billion “Recovery Fund”. While funds on the Recovery Fund are currently being disbursed, the ECB has also rised interest rates notably, while it has also started to experiment with balance sheet run off, i.e. quantitative tightening.

Figure 1. The balance sheet of the Federal Reserve. Source: GnS Economics, St. Louis Fed

Figure 1. The balance sheet of the Federal Reserve. Source: GnS Economics, St. Louis Fed

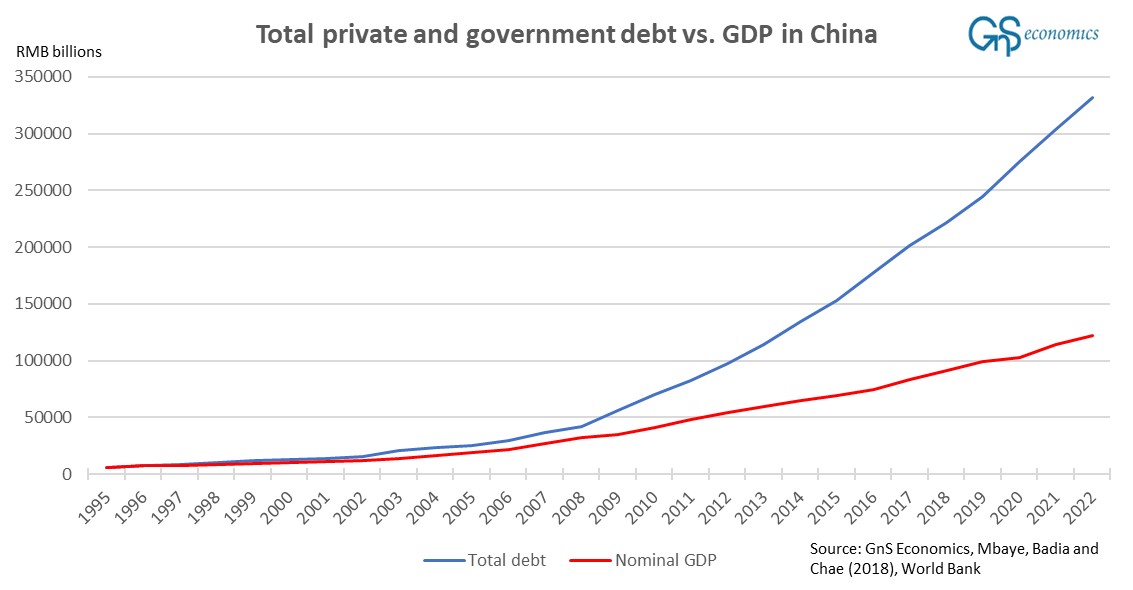

China also enacted a massive stimulus programs in March 2020, which were kept running through 2020 (see Figure 2). In 2021, Beijing enacted yet another deleveraging effort which ended in late summer 2022. Already before this, Chinese economy had become massively bloated in debt.

Figure 2. The private and central government debt and nominal gross domestic product in China.

It is obvious that such a “Ponzi-scheme”, where a linear growth of GDP is achieved through an exponential growth of debt, cannot sustain itself indefinitely. Eventually, the lending spree will lead to an impasse, where households, companies, commercial banks and entities in the shadow banking sector will not, or cannot, absorb any more debt. A debt saturation appears. China, most likely, is now at that point, as the major debt-stimulus Beijing ran between February-April failed to re-invigorate rapid growth of the Chinese economy.

The above mentioned measures created hordes of so called zombie corporations, which survive only through cheap and plentifully available credit. An era, which has now ended, and it shows.

Alas, we are closing a point of meltdown, again. The most aggressive rate hiking cycle in the history of the Fed, continuing asset run-off, approaching recession and the Flood of corporate bankruptcies that has now started are likely to push asset markets into a ‘tailspin’.

The Flood

In December 2019, we asserted that the so-called “zombie” corporations, faced with collapsing global economic demand will start to fail on a scale unseen in decades. Unemployment will skyrocket and tax revenues will collapse.

When the coronavirus erupted in early 2020, leading to lockdowns across the globe, the world economy was confronted by an unexpected and artificial depression. This naturally would have been enough to topple zombie corporations, but the situation was salvaged by massive government stimulus programs and central bank support of enterprises.

Through these measures, the probable evolution of the shock of lockdowns and pandemic into a global banking and economic crisis was stopped. However, the price of these drastic measures was that they created hordes of zombie corporations across the globe. Alas, the zombification problem was exacerbated as a result of these interventions, and now the day of reckoning has arrived.

In August, the U.S. saw the busiest bankruptcy filings on record, while U.S. companies are currently filing for bankruptcy at the fastest pace since 2020. Europe, on the other hand, witnessed the highest number of bankruptcy filings, since 2015, during the second quarter. A wide-spread corporate bankruptcies and defaults pose another major threat to the U.S. banking sector.

Banking system issue have re-surfaced in the U.S. with Citizen’s Bank, N.A., Iowa failing and taken over by the Federal Deposit Insurance Corporation, FDIC, late past week. This is what we have been warning would happen since, basically, the start of the U.S. banking crisis in mid-March.

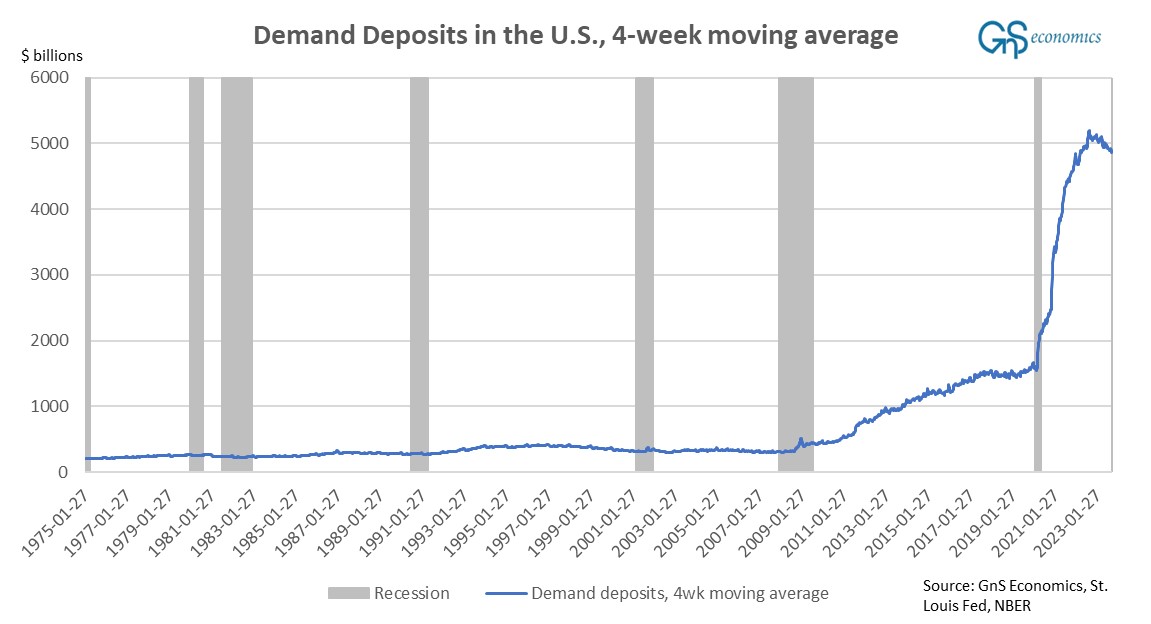

The U.S. banking sector is facing three serious headwinds. First was the collapse in the value of their main collateral, U.S. Treasuries, authorities essentially forced the banks to acquire and hold. The second is the threat of a cataclysmic bank run. The Corona lockdows combined with the stimulus checks and the massive money printing by the Fed led to an astronomical increase in the amount of easily withdrawable demand deposits in the U.S. banking system.

Figure 3. Demand deposits, or deposits that can be withdrawn any time without any prenotification in the U.S. banking system. Source: GnS Economics, St. Louis Fed, NBER.

Figure 3. Demand deposits, or deposits that can be withdrawn any time without any prenotification in the U.S. banking system. Source: GnS Economics, St. Louis Fed, NBER.Third are the massive losses tied to loans given to the real estate sector, which have been souring in the balance sheets of banks since the lockdowns. Moreover, regional banks hold a vast majority , close to $2000 billion or 66% of real estate loans. The losses from Treasuries and real estate loans combined with a major bank run could bring about an outright collapse of the U.S. banking system, which would naturally spread across the world.

It’s very likely that, when the global recession begins, the global banking crisis will resurface with renewed fervor (ála the 1930s). This would, most likely, lead to an economic calamity.

The Calamity

Due to both crashing capital markets and bank failures, joblessness and poverty would be likely to explode. Simultaneously, government tax revenues would collapse as incomes retreat and capital gains evaporate.

As governments spending skyrockets in an orgy of Keynesian counter-cyclicality, national deficits would hit all-time highs on both an absolute and relative basis. A spree of sovereign defaults would rock the capital markets.

Governments would try to save critically-important banks, which would require large-scale funding many countries—such as those in the Eurozone—cannot afford and would not be able to finance in paralyzed capital markets. This economic reality makes depositor bail-ins the only, if politically-unpalatable, option. Confronted by new and harsh fiscal realities, pensions and other social security programs would be likely to face serious cutbacks, by desperate governments.

In addition, we are threatened by another war in the Middle-East. The brutal attack of Hamas to Israel may lead to an all-out war in the region, with many “unknown unknowns”. However, if war erupts, it’s likely to spread and to crash the financial markets, re-hasten inflation (considerably) and push Europe to another, and more severe energy crisis.

A wider war in the region could lead to an outright global stagflation, where economy stalls, while inflation runs rampant. It would be a ‘double-whammy’ to the highly indebted corporate sector.

Demand would vanish, while renewed price uncertainty and higher interest rates cause wide-reaching defaults across the global corporate sector. This would, first, accelerate the corporate bankruptcies further, followed by household bankruptcies, leading rapidly into bank failures.

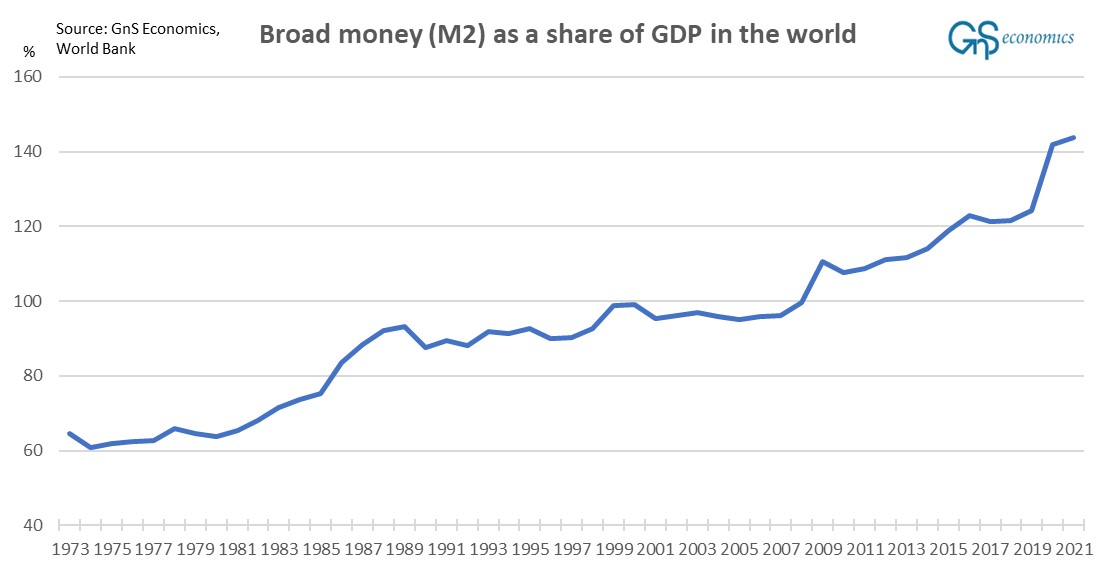

This would be likely to be followed by an utter monetary policy “perversion”, where central banks would be rising interest rates, while at the same time buying government bonds and even corporate debt (and stocks) to keep the markets from collapsing. As such a bailout would need to run in the trillions of USD, it would lead to a rapid increase in the supply of money (once again).

Figure 4. The share of broad money (M2 money aggregate) of the gross domestic product of the world. Source: GnS Economics, World Bank.

This could (would be likely to) create a situation, where the amount of money in the economy increases very rapidly, again, while production capabilities dimish. In history, such a combination has often led to hyperinflation.

Hyperinflation emerges, when there is

- Excessive growth of money in circulation.

- A broad reduction in productive capacity.

Production capacities are hampered by forces that push companies into bankruptcy. One of the most historically common and pernicious is war, such as the Great War which contributed to the hyperinflation in the Weimar Republic between 1919-1924, or the economic crash caused by the collapse of the ruling Communist political system, which preceded the Russian hyperinflation in the early 1990s. In each case, there was first a flood of corporate failures and then an effort to save the economy by creating vast amounts of money through central banks and/or through lending from commercial banks (supported and encouraged by governments and central banks) to sustain consumption.

Essentially, hyperinflation emerges, when (monetary) demand of products and services heavily outpaces their (diminishing) production. This means that there’s way too much money in circulation with respect to the production capacity of the economy. This leads to a collapse in the trust of ordinary citizens, and corporations, on the purchasing power of money. They try to get rid of the money as soon as possible, which worsens the over-demand in the economy, leading to even more rapidly rising prices. Companies start to rise their prices very rapidly in face of rapidly rising costs. This leads inflation expectation to skyrocket, with workers demanding gargantuan wage rises. Inflation simply explodes.

A war in the Middle-East has the capacity to push us into hyperinflation, IF it is followed by massive central bank money printing (like in the spring of 2020). Note also that extreme inflation episodes can be stopped only by abruptly curtailing the flow of credit into the economy, and possibly by changing the currency used within the country concerned. See our (economic) worst-case scenario for the Isreali-Hamas/Palestine conflict, as envisaged by our CEO Tuomas Malinen, for further details.

The Recovery

If the full socialization of our economies and financial markets, by central banks, does not occur (nor does WWIII), we expect the global depression to last 3-5 years. The initial collapse is likely to be over within three years (2024-2026). This, naturally, depends heavily on the path the conflict in the Middle-East takes.

The path to recovery will depend crucially on how far the ‘cleansing’ of the economy, markets and financial sector is allowed to go. If the banking sector implodes completely, the economic deficit will naturally be made much deeper leading to a systemic crisis.

However, if the essential functions of the banking sector are sustained, we could avoid the deepest malaise. Moreover, if unsound banks and “zombie” corporations are allowed to go under or are wound-down methodically, it will clear much of the malinvestment from the economy, creating the foundation for a strong and sustained recovery.

So, if we manage to return to the principles of the market economy including, most crucially, a return to undistorted price discovery in the capital markets, we are likely to see one of the most powerful recoveries in global economic history. It would be led by robotization and general technological innovation, which hard economic times tend to foster.

Additionally, debt monetization, helicopter drops, CBDC, and other money-conjuring and take-over schemes would corrupt the economy, further making a sustained recovery impossible. This is something we may face deeper in the crisis, as authorities are likely to panic.

Moreover, with the governments and the central banks assuming a much bigger role in the economy and society in this darker scenario, some form of fascism (which is, by definition, the merger of state and corporate power) would be the likely end-result of these developments. We can do nothing more than hope that wise, courageous and far-sighted political leadership will spare us from that horrible fate.

The next stage looms

As explained above, it became apparent during the spring that the Chinese economy has become saturated with debt. Households and corporations are simply unable, or unwilling, to grow their debt pile much further. This implies that we cannot rely on Chinese debt-stimulus to lift the world economy from an economic slump. When the crisis commences, it will, most likely, evolve into a repetition of the Great Depression of the 1930s leading to an economic Calamity. Unfortunately, even a worse option exists with WWIII and hyperinflation.

We are entering into a very painful era in the economic history of the world. Uncertainty in the world has probably not been higher since the Second World War, with massive economic and political risks abound. We urge you to keep preparing.

To note. It’s very rarely a bad idea to vocally demand peace ubto the world. We are at a phase, where peace is sorely needed and where every voice counts. So, don’t hold it back!

More information

We monitor the path of the crisis closely in our Newsletter, which includes event-related alerts on developments threatening the markets. In the newsletter, we also educate you how to prepare for and survive from the economic collapse.