The sudden and fast rise in the London Interbank Offered Rate (Libor), has stirred a lively debate. Its suggested drivers include rising outflow pressures on dollar deposits, an increase in short-term Treasury bill issuance, elevated credit spreads for banks and risk premiums for uncertainty towards US monetary policy. While all these deserve merit, we argue that the most prominent driver is the drastic change in policy of the central banks.

Quantitative tightening, or QT -program of the Fed, which started in earnest in January, has been altering the landscape of financial markets since October. In October, the Fed unwind first patches of Treasury bills and mortgage backed securities from its balance sheet without repatriating them with similar amounts of new assets. In January, the pace of unwind accelerated to $20 billion a month.

QT is such a game-changing event for the financial markets for the simple reason that it is a mirror-image of the asset purchase program, or quantitative easing (QE), which had a large effect on the financial markets around the globe (see, e.g., this, this, this and this) and on banking. QT programs will alter the risk allocation, which is now already visible in the stock markets and in the Libor.

The Libor fallacy

The Libor is a compilation of responses of banks to the question: “At what rate could you borrow funds, were you to do so by asking for and then accepting inter-bank offers in a reasonable market size just prior to 11 am?” Libor is thus an estimate on short term rates on uncovered loans banks use to settle transactions in their respective currencies as well as transactions denominated in other currencies. It tends to follow the interest rates set by central banks, which determines the rate financial institutions can get money short-term (over-night).

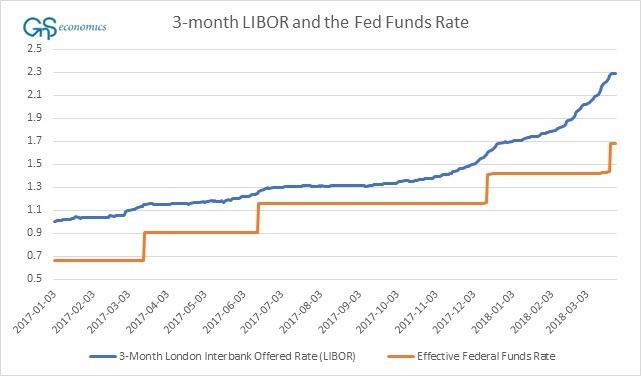

When the Libor rises notably faster than the risk-free rate (see Figure 1), it signals that the banks do not trust each other so that they would extend any longer inter-bank loans. During the 2008 crisis, Libor was in practice discontinued, because the long-term lending ceased completely. Now, the three month Libor spread over the over-night index swap (OIS) has reached levels not seen since May 2009. What makes this particularly puzzling is that other commonly used stress metrics of the credit markets, like the TED spread (3M Libor vs. 3M US Treasury bill), have risen only mildly.

Figure 1. 3-month London Interbank Offered Rate (LIBOR) and the Effective Fed Funds Rate. Source: GnS Economics, St. Louis Fed

QT, risk premium and the financial markets

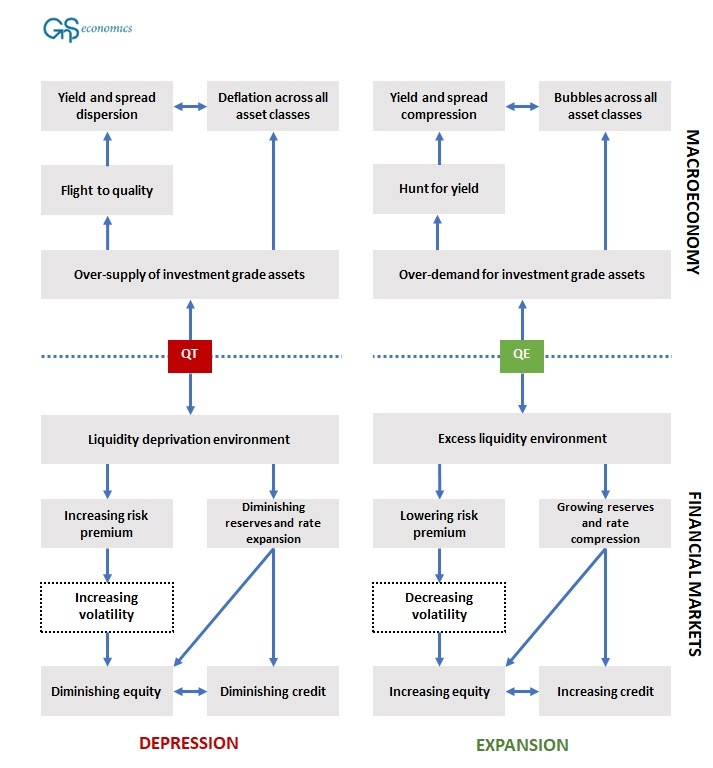

QE created an over-demand for investment grade assets and thus an excess liquidity environment in the financial markets by introducing a persistent buyer (the central bank). The over-demand led to a hunt for yield, spread compression and to inflation across the asset universe (see Figure 2). Moreover, because QE forced banks to hold high supply of reserves, they bid up various securities and made additional loans until the marginal benefit of assets in banks’ portfolios were restored to balance. This changed the reserves, asset allocation and lending in the whole banking system. Because of the vast quantities of excess reserves and liquidity in the banking system, the risk of lending to other banks was minimized.

QT will create an over-supply of investment grade bonds leading to a flight to quality, spread dispersion and asset price deflation (see Figure 2). QT removes the excess liquidity from the financial markets created by the QE by introducing a persistent seller. This will balance the risk premium, that is, the return on an investment is expected to yield more than the risk-free rate of return. It also alters the asset portfolios of banks and eventually start to shrink their reserves. This affects consumer and business lending and the lending activity of banks in the inter-bank and money markets. Risk pricing returns and rates rise, which is now visible in Libor.

Figure 2. The causative channels of quantitative easing and quantitative tightening. Source: GnS Economics

The acceleration in Libor-OIS three month spread started in November 2017 by a rapid uptick in Libor, approximately a month after the Fed started its QT, rate (see Figure 1). On the question, about why the other measures of financial stress have not risen in pace of Libor, the answer may lie in the dual nature of the QT -program (see Figure 2). When the Fed rolls off assets from its balance sheet, it creates an over-supply of US Treasuries thus lowering their price and removing the excess liquidity from the financial markets. If there is mistrust in the money markets, the receding liquidity makes it visible again. This leads to rising yields of the US treasuries and to rising Libor -rates. Therefore, because QT does not alter the OIS rates set by the Fed but it does increase the yields of US treasuries, the exposed mistrust in the money markets may widen the Libor-OIS spread but leave the other stress metrics, like the TED spread, unchanged.

After the 2008-crisis, it was the intention of the central banks to keep the money market rates low, that is, close to over-night swap rate using QE and other non-standard monetary policy measures. Now, as the blanket of central bank liquidity recedes, it will reveal the real cost and the risk in the inter-bank lending. We thus face the question whether the money markets really recovered after the crisis? If one looks at the European banking sector, the conclusion is that they didn’t. The credit default swaps of banks have also started to rise although from very low levels, thus signaling increasing stress.

The road to ruin

The return of market volatility and the rise in Libor signal that the balance sheet normalization of central banks will not go smoothly. Tremors are already felt in the stock market even though the Fed has slashed just around 1.5 % of its asset holdings. One can imagine what will happen when the ECB and the other central banks hop the wagon. Because of the multitude and the self-enforcing effects of QT on the financial markets, a complete capital market meltdown is not some distant possibility. It is a frightfully likely scenario.

However, while the timetable, announced after the FOMC meeting in September 20, states that the Fed should have slashed around $90 billion of its asset holdings by the end of March, they have actually shrunk by only $71 billion (and by only $5 billion last month). One can only speculate what has been the reason behind this, but we can safely assume that the market turbulence has played some role. For the asset markets, a lot depends on this month, because the pace of unwinding should quicken to $30 billion per month.

Despite the tinkering by the Fed, the fact remains that central bankers are between a rock and a hard place. Not trying to normalize their balance sheets and tighten the monetary policy would mean that they would have no (reasonable) means to fight the next recession. Tightening, on the other hand, is likely to crash the asset markets and possibly trigger the recession. Neither of these options will be beneficial for the asset markets. Thus, it is best to buckle up.

Download the full report describing the effects of QE and QT on the real economy and on the financial markets from our Publications -page.